The countries with the most billionaires in the world, gathered in a graph with a surprising winner

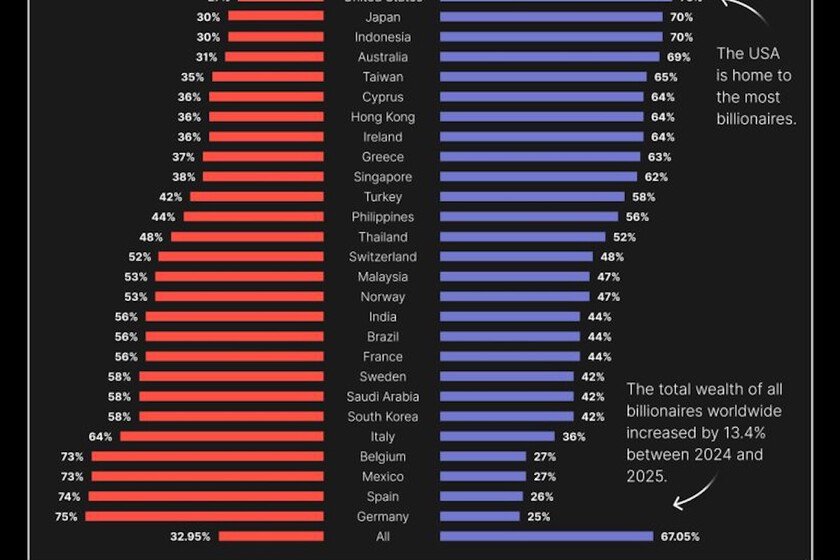

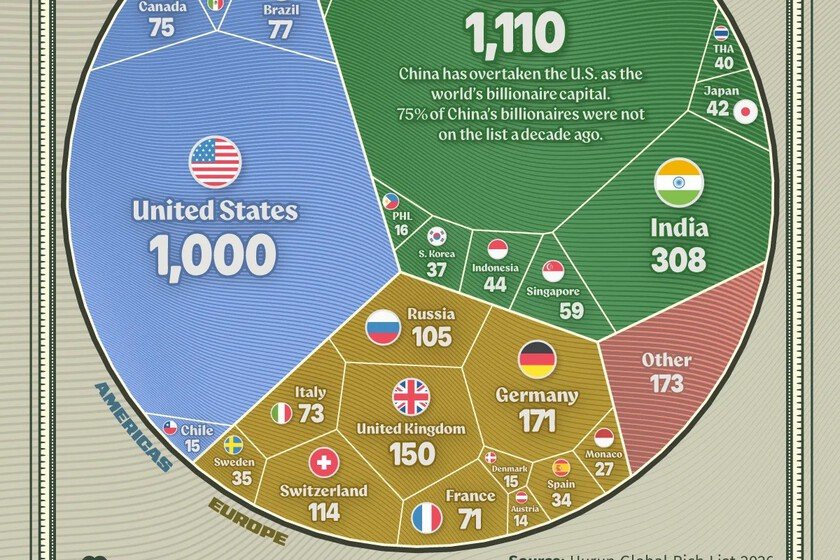

Guess, guess: Where do the majority of the world’s billionaires live today? Answer the first thing that comes to mind and without cheating. Probably most of us would say that the United States and the reality is that this was true until very recently, but the map of wealth has changed: China has just snatched the throne and already has 1,110 Chinese billionaires compared to 1,100 Americans, according to the latest Hurun Global list. The most striking thing is not so much this surprise, but the speed at which it has happened: a decade ago, three of those four Chinese billionaires were not even on the list, which gives an idea of the industrial, technological and business panorama of the Asian giant. Of course, the “land of opportunity” thing seems to have changed zip codes. The Hurun Global Rich List 2026 is an annual ranking prepared in China that has been measuring the fortune of the world’s billionaires for 15 years. It is not as popular as Forbes, but it is also one of the great references for quantifying billionaires. Both estimate net worth in dollars based on shares in listed companies, real estate and other assets, but each has its own methodologies, so there may be divergences between the two. The list is not very intuitive to visualize, so Visual Capitalist, through its Voronoi data platform, has prepared this graph that reflects how many billionaires (in dollars) live in each country in the world in 2026. We have already discovered gold and silver, but there is another curious fact: China and the United States alone concentrate more than half of the global billionaire population. To the surprise of few, wealth is concentrated. Beyond statistical curiosity, there are two reasons why it is interesting to know where the rich are concentrated: according to Oxfambillionaires are 4,000 times more likely to reach political office than the average person. Simply put: wealth is concentrated and it also tends to concentrate power. On the other hand, global billionaire wealth grew more than 16% in 2025, three times more than the average of the last five years, according to Oxfam. The rich are getting richer. The countries with the most billionaires in the world After China and the United States, India is at a certain distance but far away from the rest of the European squad, with 308 people. And the old continent already appears, with Germany (171), the United Kingdom (150), Switzerland (114), Russia (105), among others. According to Hurun, China added 287 billionaires compared to the previous year, compared to 130 in the United States and 24 in India, which explains why the list has changed so much. Spain appears in 20th place with 34 billionaires, behind countries of comparable or smaller economic size such as Sweden or Turkey and an abysmal distance from Switzerland, which has 114 and a trick to achieve it despite its small size that it shares with Monaco: favorable taxation. Where billionaires live in 2026. Visual Capitalist Where do these new billionaires come from? Although we already know that Most rich people are born and not made and the Hurun list confirms this, with 144 fourth-generation fortunes, this rise of the new rich has specific origins such as the market or technology. But technology is a very broad sector and the phenomenon that concentrates it is a boom that we have been finding in the soup for some time: artificial intelligence. Thus, there are 114 billionaires who owe their fortune to AI companies, of which 46 are newcomers to the list. Furthermore, there are countries and countries: despite representing 79% of the world’s population, Southern countries only own 31% of global wealth. In wealth there is also migration, but quite concentrated in one country: the United States. Of this 14% of “luxury” migrants there are famous cases such as those of the South African Elon Musk or the Taiwanese Jensen Huang. It is important to remember that a ranking of the number of billionaires is not the same as how rich a state is or the average well-being of the population. On the other hand, the country of residence can sometimes be somewhat ambiguous: some billionaires have dual tax residence or assets distributed internationally and both the geographic allocation criteria and the estimation of their assets may differ from Hurun compared to other sources. In Xataka | Tell me where you are from and I will tell you if the rich in your country were self-made or inherited wealth In Xataka | Where the ultra-rich are growing the most: the graph that proves that Europe is playing something else