The most profitable action of the AI revolution in Spain is not a software company. It is a construction company

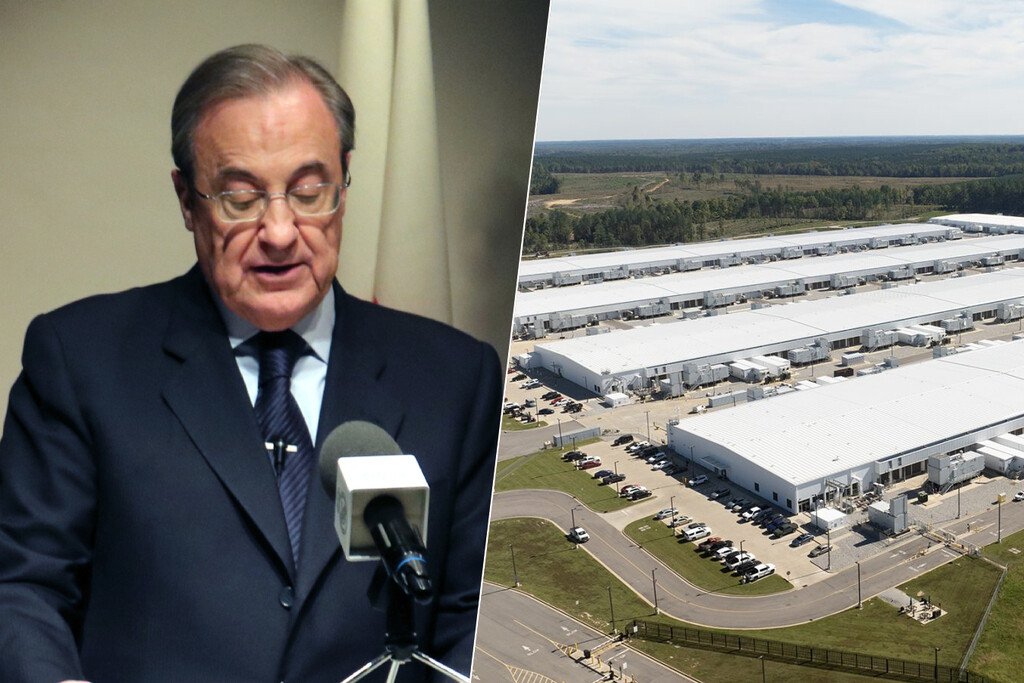

We know Florentino Pérez ample by hire galactics and for his business successes, but a priori we would not easily relate him to the rise of AI. And by not doing so we would make a serious mistake, because the manager managed to see before anyone else that this was a huge opportunity… and he is taking advantage of it almost without us realizing it. what has happened. ACS is a construction company that doesn’t seem particularly fascinating. You lay bricks, asphalt and cement, but in 2025 the data tells a fascinating story. The company obtained a net profit of 950 million euros, 15% more than the previous year, and the engine of that growth was its American subsidiary, Turnerwhose contribution to the group’s results grew by 66.6% to 549 million euros. Turner doesn’t build flats or highways. Build data centers. And therein lies the crux of the matter. AI needs big construction companies. The transformation has not happened all at once. ACS has been betting on this niche for years with a simple but powerful thesis: AI requires enormous amounts of hardware, and that hardware needs equally huge buildings with cooling, energy and security. And ACS is dedicated to precisely that: to build large buildings. In Xataka Amazon is building an empire in Aragon: it has just paid 1.5 million to expand the electrical network to its fifth data center Florentino triumphs in the US. Turner arrived earlier and stronger. In 2025, ACS won several large-scale data center contracts, including the construction of a 902-megawatt center in Wisconsin as part of the Stargate program, and a stake in the $10 billion, one-megawatt Meta campus in Indiana. Those are conventional projects. They are cities whose inhabitants are servants for this new era of AI. Go for it all. As they point out in five daysdata centers generated more than 9 billion euros in sales during 2025, and ACS has already delivered more than 9 GW of capacity all over the world. That figure is extraordinary, especially considering that in all of Spain the installed capacity barely reaches 7 GW. The Spanish company that talks the least about AI has been silently one of its great beneficiaries for years. Very much in the style of Florentino Pérez, who usually maintains a relatively low profile and succeeds without making too much noise. Stocks on the rise. The market took a while to see it, but it has reacted forcefully. ACS shares have soared 115% in the last twelve months. Today they are close to 110 euros and mark historical highs while the construction sector advances (“only”) 20%. Group sales they reached 49,848 million euros, with the US and Canada contributing 63% of the total. ACS is in practice more of a North American technological infrastructure company than a Spanish construction company. It is listed on the Ibex and is chaired by one of the great football personalities, yes, but its current driving force is not here, but in the US and in the AI fever. Build and Own. ACS is not limited to executing other people’s contracts: it also wants to be the owner of what it builds. In January 2026, the company completed an alliance with Global Infrastructure Partners, BlackRock subsidiaryto create a 50/50 joint venture to develop a global data center platform with an initial capacity of 1.7 GW. Already before had bought Dornanan Irish engineering company specialized in this type of infrastructure, for 436 million euros. ACS doesn’t just want to build AI data centers: it wants to own a piece of that infrastructure. The dollar as a great risk. One of the big problems with this project is the US currency. With more than 60% of its income in North America, each fall of the dollar against the euro is a setback for the Spanish multinational. The devaluation of the dollar is already greater than 10% after the last twelve months, and that has prevented Turner’s growth from being even greater. According to Renta 4 analysts, the “currency effect” subtracted more than five percentage points from the growth of net profit. And investors warn. Analysts themselves consider that the AI market has already discounted a good part of future growth. At Bloomberg, the consensus is to maintain the stock with an average target price of 88 euros, which would imply a fall of 20% compared to current levels. This is what usually happens with good economic stories: when everyone knows them, they are no longer an opportunity. But at ACS they are optimistic. Although experts are cautious, at ACS they expect that spending on infrastructure quadruples from now to 2034. In fact, they expect that the benefits of 2026 will go even further than those of 2025 and exceed 1,000 million euros. If it achieves this, Florentino’s company will have completed one of the quietest and most profitable industrial transformations in the recent history of our country. {“videoId”:”x86aas4″,”autoplay”:false,”title”:”60% of the INTERNET passes through HERE: This is the LARGEST Data Processing Center in SPAIN”, “tag”:””, “duration”:”266″} Turner is ahead. According to Data Center MagazineTurner accumulated a backlog – a portfolio of confirmed orders – of $39 billion as of August 2025. It is the dominant construction company in this segment globally, although of course it has direct competitors such as DPR Construction, Holder, Skanska or AECOM. However, none have achieved the same concentration of contracts with the hyperscalers (Meta, Amazon and Microsoft). Turner has been building its reputation as a builder of this type of facility for more than a decade, and it is very difficult to replicate that advantage quickly. The irony of ACS and Spain. There is a geographical paradox in this success story: Spain and Europe have years debating on digital sovereignty, technological dependence and the need to build own infrastructure for not to be left out of the AI revolution. While this debate is taking place, the Spanish company that is most building this infrastructure is doing so almost exclusively outside of Spain. As … Read more