Because of climate change, by 2100 we will lose the equivalent of what 2 billion people eat each year in crops.

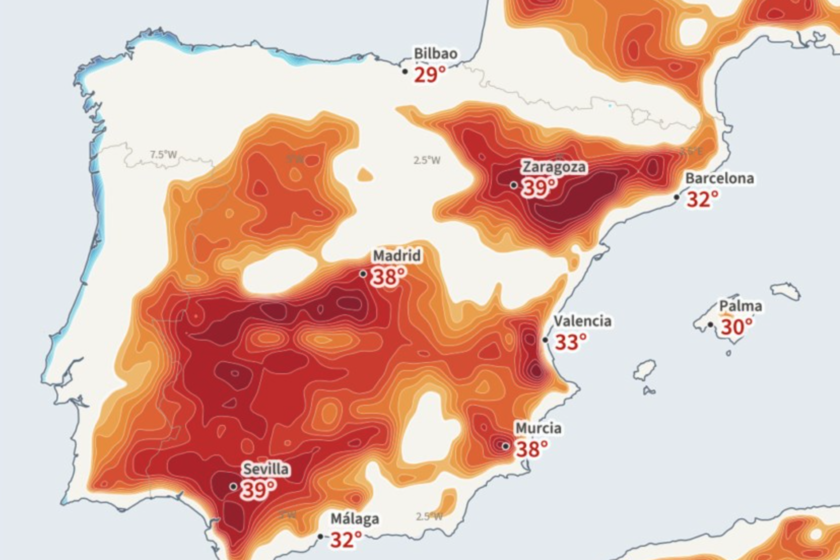

We all know that climate change affects crops. the drought, global warmingextreme rainfall and many other related weather phenomena can seriously endanger agricultural activities. Given that these are the main livelihood of millions of people around the world, it is a situation that is worth analyzing carefully. It is precisely what has done recently a team of scientists from the International Institute for Applied Systems Analysis (IIASA) in Austria. After comparing historical episodes of extreme heat with crop yield data from the FAO, they observed that we have been gradually losing crops for several years and that this, as climate change progresses, will only get worse. So much so that by 2100 losses of 160 billion dollars annually are estimated. Only three crops. The situation is even more worrying if we take into account that the data has been analyzed for only three crops: cornsoybeans and wheat. These were selected because there was sufficient data from FAO to carry out both phases of the statistical analysis. The first, calibration, was carried out with data from 1974 to 2004. On the one hand, historical records on episodes of extreme heat and drought were taken and then they were confronted with the existing information on the yields of these crops in different countries around the world. Thus, it was possible to obtain a formula on the correlation between climate and crops. This formula was then validated with data from 2007 to 2019. The objective was, with the climate information for that period, to calculate how it would affect crop yields. For the validation to be positive, the results should coincide with the true performance that was recorded at that time. And so it was. The data coincided and were not at all encouraging, as the first losses began to be detected. Specifically, there was a 3.5% decrease in crop yields. It may seem like little, but as explained to New Scientist one of the authors of the study, Kai Kornhuber, are relevant figures about a global impact, which could even trigger serious crises at a regional level. In fact, there are already annual losses of 20 billion dollars. A worrying situation in 2100. With the model already validated with known data, these scientists ventured to analyze an unknown future. What they saw when entering data for a scenario high emissionswith current trends, was very worrying. According to their calculations, global yields will fall by around 35% by 2100, with annual losses exceeding $161 billion. Another of the authors of the research, Yi Ling Hwong, explained in May at a meeting of the European Geosciences Union that the losses would be roughly equivalent to what around 2 billion people consume in a year. Crops affected by climate change around the world. The calculations have been made at a global level. There would be losses in all countries, including developed ones. However, these scientists warn that the situation will be especially serious in developing countries, where many people depend on agriculture for their livelihood. It can be solved. The positive part of all this is that, according to the authors of the study, you can try not to reach those figures. Kornhuber recalls that climate scientists make these statistical calculations with the goal of making people react and their predictions ending up being wrong. Therefore, they hope that this data will be disseminated and will help farmers to find ways to adapt, choosing new crops, according to the climatic conditions of each area and customizing irrigation. Limitations. This study on how climate change affects crops has limitations that must be recognized. Firstly, only three crops have been calculated. Others could be related to worse or better data, so it cannot be extrapolated to everything that grows on earth. On the other hand, only climate data related to extreme heat and drought are taken into account, but not with the floods or hail, for example. These are also phenomena associated with climate change that affect crops to a large extent. In addition, some scientists outside the study consider that the statistical calculations used may be good for making short-term forecasts, but not for the end of the century. Some even believe that the data may be overestimated. Even so, the authors of the study insist that it is better to be somewhat alarmist so that measures are taken than to underestimate the data and, with the truth in the face, it is too late to take action on the matter. Because that is the great reality of all this. Something has to be done. Data can be the push needed to get started once and for all. Image | Magnificent In Xataka | Google has shown with its AI that the prediction of storms and hurricanes is outdated. This is how your new model works