The European Bizum will soon be a reality. It is very bad news for VISA and Matercard

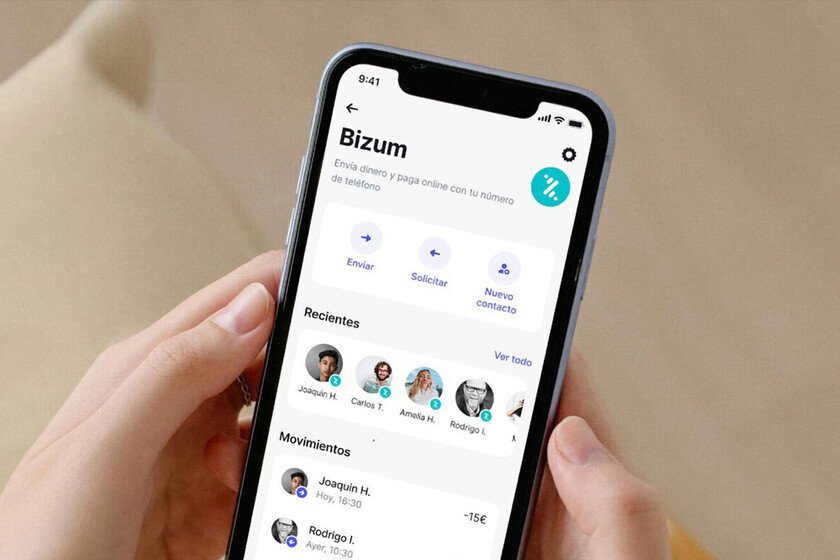

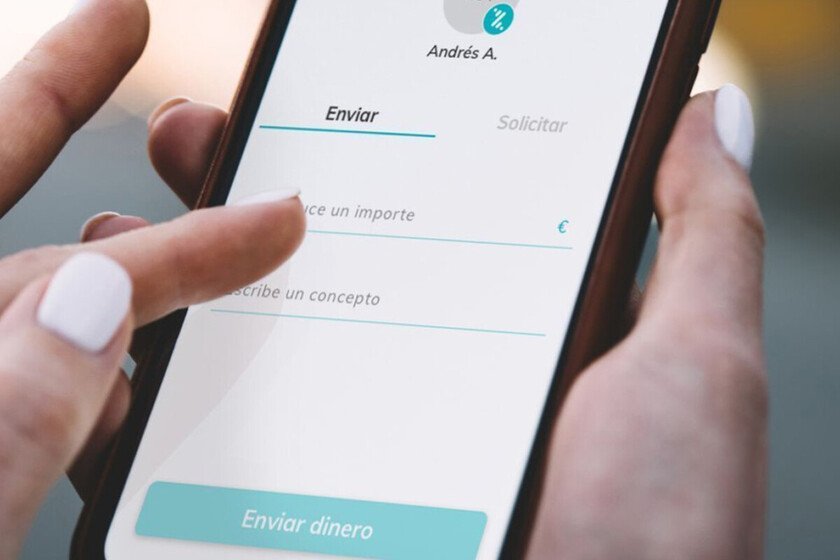

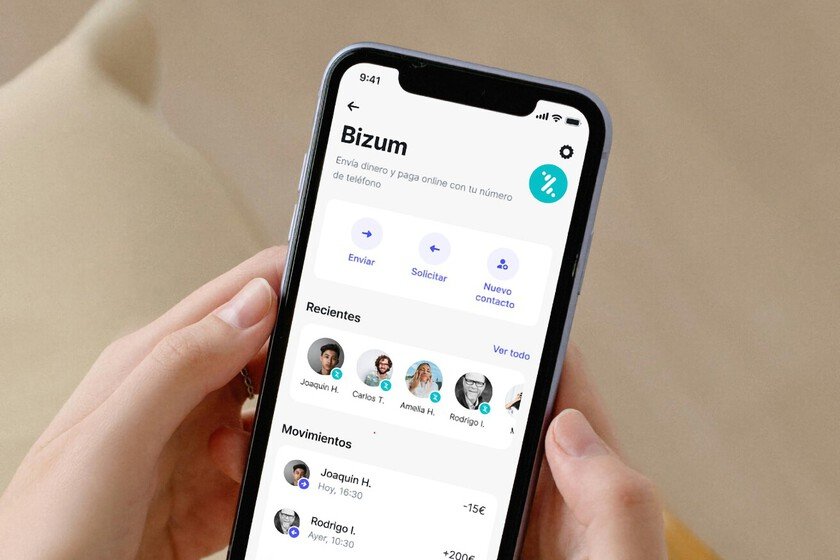

Europe will have its pan-European mobile payment system. Although we all thought that we would have a unique and universal Bizum For EU countries, what will happen will be a little different, but just as effective and probably better: long live interoperability. European Bizums connect. As indicated in CincoDíasBizum and the rest of the European platforms that imitated those free transfer functions easily accessible from mobile phones have finally joined forces. all friends. That was the last obstaclebecause all of them wanted to become the unique and universal Bizum. That would have forced the rest of the platforms to say goodbye to make way for that single platform, but instead what will happen is that the different platforms will be interoperable. The agreement includes 130 million connected users. Thanks to this interoperability project, 130 million EU (and Norwegian) citizens will be able to use this system. Not only that: the interoperable platform will be prepared to accept those from other European countries such as Switzerland or even others from markets not belonging to the euro zone. The key is in SPL. This interoperability can be achieved thanks to the so-called Standard Proxy Lookup (SPL), a “directory” service at the European level managed by the European Payments Council (EPC). This service allows banks to check which IBAN corresponds to each telephone number. Everything runs on the SEPA Instant Transfer infrastructureand thanks to new EU regulations, these transfers will soon be mandatory free or will have the same cost as a standard transfer, eliminating the traditional abusive commissions for immediate transfers. In 2026, personal payments. The technical implementation will begin in the coming months, and it is expected that before the end of the year a Spaniard with Bizum will be able to send money to a German with Wero and vice versa in a transparent and simple way. In theory, the operation of the system will not change for users, who will simply have to enter the recipient’s mobile number, regardless of the EU country, so that the transfer is carried out instantly. Shops in 2027. These personal payments with the European Bizum will end up giving rise to the other great option of the system: payments in electronic stores and points of sale. This option will arrive a little later, in 2027, and will undoubtedly be the great spearhead of these platforms against the two fierce competitors that dominated this segment. Setback for Visa and Mastercard. This agreement allows the European Union to have an internal payment system that will allow it to reduce its dependence on the systems that have been the de facto industry standard for decades, those offered by Visa and Mastercard. And a measure of the banks for the banks. European banks are also strengthening their position regarding the digital euro project that the European Central Bank (ECB) is preparing. This currency will in the future allow European citizens to have deposits in central banks without intervention by private banks. That, of course, took power away from these entities, but with this European Bizum they reinforce their role. Another step towards European digital sovereignty. For decades Europe has delegated all its digital systems to companies, especially from the US, and this project confirms an increasingly strong trend: that of European digital sovereignty. When processing payments within a European banking network, citizens’ consumption data does not go to US servers (as happens when using Visa, Mastercard, Apple or Google). And you can use Bizum without a bank card. This agreement does not prevent the platforms from continuing to evolve and improve on their own. This is what Bizum intends to do, which will launch Bizum Pay this year to pay directly in stores with the current account and without the need for a bank card. This will allow us to avoid dependence on Google Pay or Apple Pay, for example, on our mobile phones. It will first offer this option in shops in Spain, and in 2027, in line with the objective of that interoperable European Bizum, in shops in the EU. In Xataka | The Treasury confirms it: payments for dinner and gifts to your friends through Bizum do not go to the Tax Agency