Revolut accumulates 6 million customers in Spain. Trade Republic has doubled its own in ten months. When Revolut grants mortgages, we will talk about a war that escalates.

Why is it important. It is not common for actors outside the system to appear in a sector as large and historic as banking (without a network of branches or lobby nor the level of advertising of the large ones) and achieve a scale comparable to that of medium-sized entities, in a very short time.

They have also done so by attracting younger clients with a greater propensity to operate: exactly the profile that generates the most commissions and that is most difficult for traditional banks to recover.

The context. Spain has been a seemingly impenetrable financial market for years: highly banked, highly concentrated after the 2008 crisis and dominated by four or five entities that control the majority of the retail business.

The digital commitment of big banks (Imagin from CaixaBank or Openbank from Santander) is working well, but the essence of the matter has not changed: they are subsidiary brands that do not threaten the core business of their parent companies. Revolut and Trade Republic, on the other hand, are independent entities with no internal conflict to resolve.

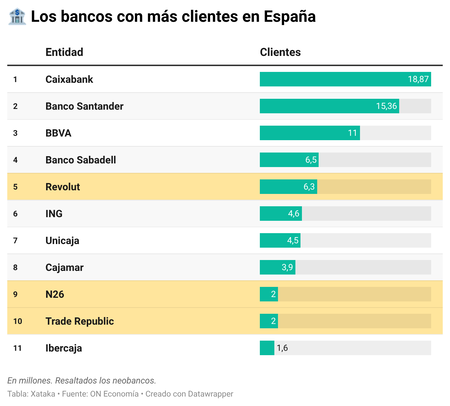

In figures:

- More than 6 million Revolut customers in Spain at the end of 2025, with a penetration of 13% of the population, close to ING and ahead of Banco Sabadell.

- 3,990 million euros in total Revolut deposits in Spain according to the Bank of Spainwith a growth of 74% in 2025.

- 2 million Trade Republic clients in Spain, doubled in just ten months, with a projection of reach 3 million before the end of 2026.

- Spain is already Revolut’s second largest market in the EU, and the third globally, only behind the United Kingdom and France.

The two sides of the same phenomenon. Revolut and Trade Republic attack different but complementary flanks.

- Revolut is going after the everyday bank: checking account, card, currency exchange, savings, personal loans, soon business credit… and considerable success when it comes to positioning itself as a card for travel or online purchases.

- Trade Republic goes for savings and retail investing: ETFs, stocks, cryptocurrencies and a 2.75% APR interest-bearing account with no balance limit.

Together they cover practically the entire banking customer value chain retail. What used to require two or three banking relationships now fits into two applications.

Between the lines. The most revealing data about Trade Republic is the speed at which they are growing: one million new users in less than a year, a rate that exceeds that which the entity itself registered in Germany during its initial expansion. It is a sign that in Spain there is a latent demand for alternatives that traditional banking has never fully satisfied, especially among the group of savers under forty years of age.

The average age of the Trade Republic customer is around 35 years old. They are exactly the clients that IBEX banks need for their next decade.

Yes, but. Growing customers is not the same as capturing their money. Revolut has 13% penetration in Spain but barely 0.25% of the system’s total deposits, according to a Citi analysis collected by The World. Only 1% of payrolls reach Revolut. Most of its users use it as a secondary bank: for trips, for specific payments or to park some savings with better remuneration than their usual bank.

Trade Republic has not yet published its deposit figures in Spain. Traditional banking has been using this argument as a shield for some time: having many clients with a low average balance is not a business model, it is an acquisition model. The real test will come with the credit.

The decisive moment. The big unknown (and the biggest threat to conventional banking) is the mortgage. Revolut has confirmed that it plans to launch it in Spain between 2026 and 2027. The model you have announced is completely digital, without negotiation: an offer. Take it or leave it. Ignacio Zunzunegui, Revolut’s growth director for southern Europe, said this in an interview with The World: “You could press a button and start being much more aggressive with credit.”

If that works, Revolut stops being “your other bank” and becomes the first, as happened to ING in the first decade of the century.

- The mortgage is the product that anchors a client for decades, the one that generates the deepest relationship and the greatest income over time. It is the last moat that protects traditional banking.

- Meanwhile, its CEO has confirmed that Revolut will not go public before 2028: a company with almost 2,000 million euros of profit that prefers to remain unlisted publicly while it consolidates markets.

Featured image | Sophie DupauTrade Republic

In Xataka | Revolut wants more than your savings: it’s going after Spanish millionaires

GIPHY App Key not set. Please check settings