Saudi Arabia already knows the real price of Neom and it is not measured in billions, but in barrels of oil at $90

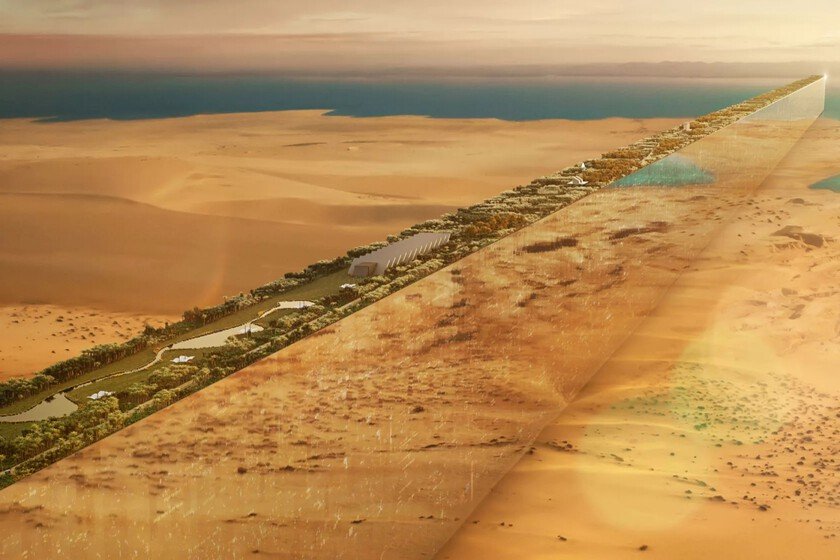

Saudi Arabia is mired in a paradox that revolves around barrels of oil. Years ago the kingdom launched an ambitious program to reduce its dependence on ‘black gold’, a key element in its accounts and public treasury. Under the name of ‘Vision 2030’ basically proposed to diversify its economy with a rosary of projects which included large urban developments such as Oxagon, Trojena or the famous The Line. The problem is that the swings in the price of crude oil (the same one from which he wants to get away) is complicating the things. So much so that the kingdom has already been forced to moderate its expectations. What has happened? We told you a few days ago: Saudi Arabia has had to rethink the Neom megaprojects, the program with which the kingdom wants to promote works such as Trojena or The Line, a futuristic city 170 km long, 500 m high and 200 meters wide built from scratch in the middle of the desert. According to Financial TimesNeom’s president, Crown Prince Mohammed bin Salman, is now considering a “much smaller” scale. In fact, there is already talk of a drastic cut in The Line and changes also in Trojena. Is it a novelty? Half. Despite the efforts of Saudi Arabia for showing how the works were progressing, the international press has been warning for some time the difficulties (technical, but especially financial) that the kingdom has encountered to carry out its projects. own FT posted a few months ago a report in which he talked about how Neom’s dream is “unraveling.” His last article It goes further however and helps to understand the context. The cuts come after Neom officials commissioned an audit of the project. And although its final conclusions are not yet known, they seem to be strong enough that there are already architects working on the redesign of The Line. Their goal: to turn it into a “modest” project that can take advantage of the infrastructure built in recent years. There is talk of a change in concept, of a Neom that (without giving up the diversification of the Saudi economy) stops focusing on the “cities of the future” to focus on something much more concrete: data centers. The kingdom insists in any case that Neom is a bet that “aims to span generations” and its discourse (at least the public) is far from being defeatist. What is the problem? Beyond the scale and enormous ambition of the projects (only The Line involves building a 170 km city), Riyadh has encountered a perfect storm. Not even her years of waste (or precisely because of them) have prevented her from being forced to rethink some milestones in her initial schedule. The clearest example Trojena leaves it. There, in its ambitious ski resort, the 2029 edition of the Winter Games was going to be held. A few days ago, however, the Asian Olympic Council and its Saudi counterpart announced that the appointment will have to be postponed indefinitely. Financial Times remember that in the medium term the kingdom also has important commitments that will require it to step on the accelerator. The first will arrive with the international fair Expo 2030. The second, with the 2034 World Cup. Click on the image to go to the tweet. And what does the oil look like? If something they usually repeat analysts trying to explain the development of Vision 2030 (and more specifically Neom) is how the price of crude oil is influencing it. The reason is very simple. Although the financing of Vision 2030 does not fall directly into the budget of Saudi Arabia, its implementation does depend on large projects funded by the State. And it receives a large part of its income through oil. Saudi Arabia is the main exporter of crude oil on the planet, which explains that in 2024 this will represent 60% of public income. In general, oil and natural gas accounted for more than 20% of its entire GDP that year. A few months ago Arab Gulg States Institute (AGSI) I remembered that the weight of the oil business in the Government’s tax revenue is today much lower than a decade ago, when it reached 88%, but it has still accounted for close to 63% in recent years. Not only that. Its technicians recognize that the health of Aramco (the Saudi national oil company) is “vital for the health” of the public coffers and the country. Why is it important? By a simple rule of three. The implementation of Vision 2030 depends largely on the Saudi kingdom and its PIF (the Public Investment Fund), sovereign in nature and chaired by Mohammed bin Salman. And the money they receive is closely linked to the progress of the global oil business. In April of last year, in a complicated context, marked by fear of the trade war and differences within OPEC, Reuters warned of how the fall in the price of crude oil would be reflected in Aramco’s dividends… and these, in turn, in the money that would enter the coffers of the Government and the PIF. “The Government and the PIF will receive 32 billion dollars and 6 billion dollars less, respectively,” collected the chronicle signed by Yousef Saba. Already at that time there were experts who pointed out that this snip would take its toll on some of the projects that the kingdom had in its hands. “Saudi Arabia is likely to depend on debt financing and will have to delay or reduce some planned contract awards,” insisted Karen Young of Columbia University, recalling the nation’s deficit. Is there more? Yes. A key fact that in recent months have slipped several analysts and in which affected these days Brad Setser, CFR researcher, following the latest news about Neom and The Line. It is not just a matter of the price of oil rising or falling in the market, it is that Saudi Arabia needs the barrel of Brent to remain at certain … Read more