Spanish banks have no problem letting you buy cryptocurrencies. What they don’t want to do is advise you on them.

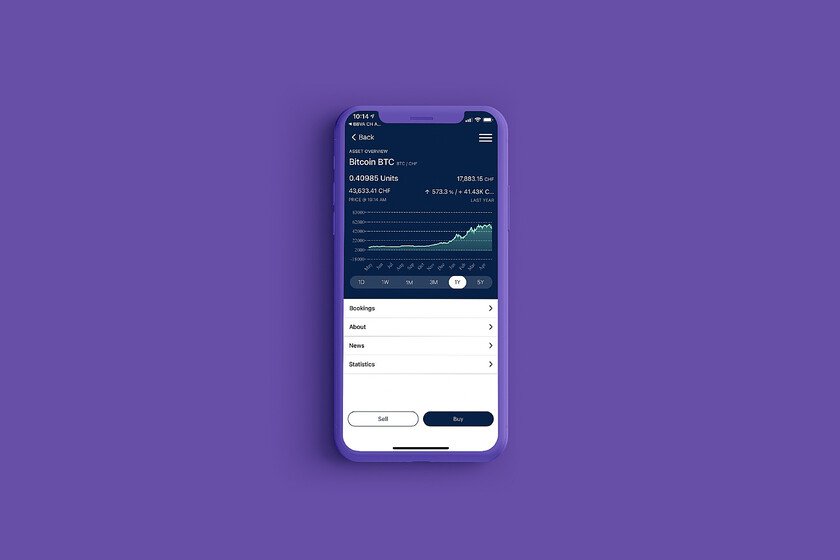

In March 2025 BBVA he stuck out his chest. It was the first large traditional bank in Spain that allowed its clients to operate in cryptocurrencies. Then other entities such as CaixaBank and OpenBank followed. In all of these cases there is a crucial detail: one thing is that they let you operate with cryptos. It’s quite another to advise you on how to do it. You cook it, you eat it. That traditional banking has made this move is definitive proof that cryptocurrencies have managed to convince even this very conservative sector. But these institutions are not willing to risk too much, so although they allow their clients to buy or sell cryptocurrencies, they leave all responsibility to the client: they do not advise or advise. And it’s not likely that they will. Nobody wants to advise. A report published by the ESMA and the EBA reveals that the vast majority of entities follow the same pattern: they allow trading with cryptocurrencies, but do not advise clients about them. Of the 110 entities that have achieved authorization of the MiCA regulation in Europe, only 20 have requested to provide crypto advice. 11 provide recommendations (like eToro) and another nine offer portfolio management. There is a clear reason why these entities leave the ball in the clients’ court. Too much risk. Caution is absolute not only on the part of traditional banking, but also of traditional exchanges or trading markets. These entities, which have traditionally been the only resource for users to operate with cryptocurrencies, have never offered advisory services, and one was clear when investing that they assumed full responsibility for their actions. The surprise is that exactly the same thing happens with traditional banking. They ignore it, and they do so because they have no interest in advising: the reputational risk is too high, and the volatility of these assets makes it especially difficult to make reliable recommendations. Crypto analyzes guarantee (almost) nothing. As explained in five days Gliroia Hernández Aler, co-founder and partner of finReg360, “Crypto assets have the value that the market assigns to them. By not having an underlying that can be analyzed, such as an income statement, for example, it is difficult to base advice on objective data. Although there is more and more news that can impact bitcoin, it is difficult to do a quantitative analysis with traditional methods.” MiCA opened the market. Europe wanted to try to regularize that “wild west” that the crypto market had become. To this end, in mid-2023 it approved the MiCA (Markets in Crypto Assets) regulation, a European regulation to regularize this activity. Among other things, it offers consumer and investor protection and establishes measures to prevent market abuses. Banks as the new exchanges. We had to wait two years to see how the first banks took advantage of this regulation, but little by little more and more entities joined in. The message was clear: you no longer have to resort to “mysterious” cryptocurrency trading markets (exchanges). You can buy at your usual bank. Image | BBVA | André Francois McKenzie In Xataka | A British man was not allowed to look for his bitcoin disk in the trash for years: now he is considering buying the landfill