Orange has confirmed that it can simultaneously undertake the purchase of 50% of Masorange and its proportional share of Altice’s assets in France without affecting the dividend. Or so he claims. Laurent Martínez, financial director, has said it unequivocally: both operations are viable while maintaining “profitability for the shareholder as an absolute priority.”

Why it is important. Five years ago, any European operator that had announced two large acquisitions in parallel would have suffered an immediate stock market punishment. Now the market digests it.

It is the first major sign that the consolidation of the sector has ceased to be a regulatory taboo and has become an accepted strategic necessity. There are even signs that Europe begins to give way after decades of anti-concentration dogma.

Between the lines:

- Orange is looking for customers and spectrum in France, not duplicate infrastructure.

- In Spain, the Masorange shareholder agreement blocks any movement until April 2026.

- But CEO Christel Heydemann has been clear: “There is no rush.”

They can wait because they have financial muscle. That capacity for patience is, in itself, a competitive advantage.

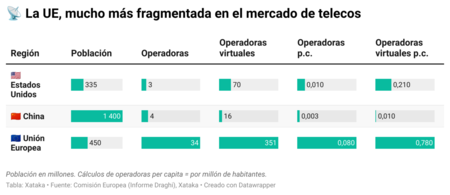

The context. Europe has 34 main operators for 450 million inhabitants. The United States has three for 335 million. China, four for 1.4 billion.

Proportionally, Europe has eight times more operators than the United States and 27 times more than China. The result: compressed margins, insufficient investment and a 41% drop in the sector’s market capitalization between 2015 and 2023.

Unexpected twist. Teresa Ribera, new European Commissioner for Competition, said in spring that the rules will “evolve” to allow for greater scale. It’s a radical departure from her predecessor, Margrethe Vestager, who systematically blocked mergers for a decade. The Draghi Report has explicitly called for facilitating consolidation. Something is moving in the bureaucracy.

Marking agenda. Marc Murtra, president of Telefónica, has led a manifesto signed by twenty European telecommunications companies calling for drastic changes in merger regulations.

It’s not rhetoric: Telefónica has liquidated its businesses in Latin America to concentrate on Europe with the addition of Brazil. Murtra has declared that the teleco “will be active in a future scenario of European mergers.” They want to be much more than the large Spanish telecom. It’s been rumored for months its interest in taking over Vodafone Spain and with the German 1&1. Digi has even sounded.

Yes, but. Not two of the three large Spanish operators can finance a state-of-the-art fiber network without external help. PremiumFiber, presented by Masorange and Vodafone A few days ago, it needed the Singapore sovereign fund with 25% of the capital.

That is the real picture: without consolidation, European telecommunications companies will increasingly depend on Asian capital to maintain competitive infrastructures.

The big question. Will Europe allow its operators to consolidate now, while they still have muscle, or will it wait for American and Chinese giants to absorb the European market piecemeal? Orange has shown that it can play on two boards at once. It remains to be seen whether regulators are going to let the game continue.

In Xataka | Telefónica wants to lead Europe. But he resists turning Spain into his letter of introduction

Featured image | Xataka, operators

GIPHY App Key not set. Please check settings