This is the Hormuz “swarm” that threatens to break the $100 barrier

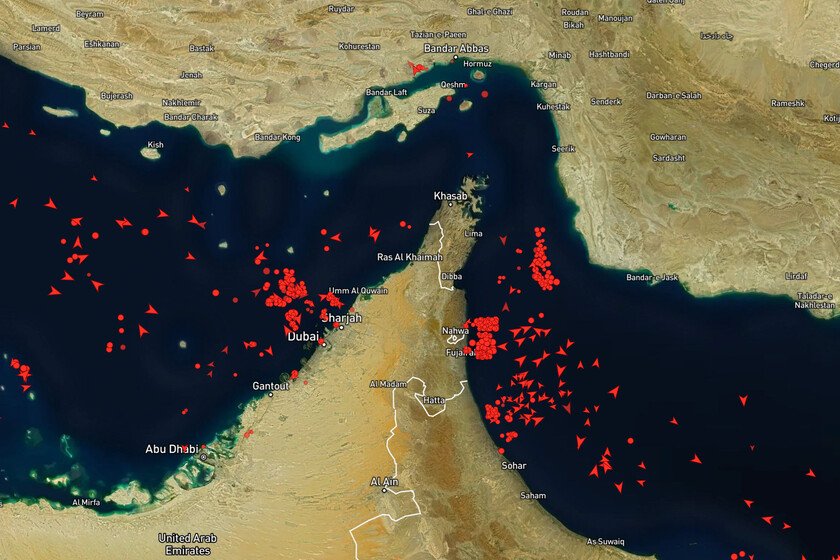

Just enter Marine Traffic to understand the magnitude of the problem. The entire world is holding its breath before a funnel of water just a few miles wide. Through the Strait of Hormuz travels approximately 20% of the world’s daily oil supply and a vital quota of liquefied natural gas (LNG). Today, that global artery is suffering a heart attack. An unprecedented escalation in the Middle East, detonated by attacks of the United States and Israel that ended the life of the Iranian supreme leader, Ayatollah Ali Khamenei, has unleashed a hail of missiles and drones. The result is a blockage de facto of the most important sea route on the planet. X-ray of a historical traffic jam. The cover image of Marine Traffic It is a veritable swarm of red icons that crowd on both sides of the strait, especially near the Iranian port of Bandar Abbas and off the coast of the United Arab Emirates. Once we move the cursor over the boats, we see that they are still. According to the data of S&P Globalmaritime traffic has plummeted, between 40% and 50%. There are around 240 ships clustered waiting for instructions. Among them, as analyst Weilun Soon details in Bloombergthere are at least 40 supertankers (VLCCs), inactive giants each loaded with about 2 million barrels of crude oil. And time is against us: according to estimates by JPMorganIf this effective closure lasts more than 25 days, producers will run out of space to store crude oil and will have to stop physical production. The chaos is not only physical, it is also electronic. The data team SkyNews has documented severe interference in ship tracking systems (AIS). The signals are so distorted that some oil tankers appear located inland on radars. The fear is more than justified: the war has already spilled into the water. According to reports from the UKMTO (UK Maritime Commercial Operations) cited by Business Insiderthe tanker skylightflying the Palauan flag, was attacked near Oman. The balance has left four injured and 20 crew members urgently evacuated. Markets in panic and freight rates through the roof. The chain reaction has not been long in coming. In a quick look at the bag, we can observe the initial panic of investors: in the first hours of operations, Brent crude oil (the European benchmark) soared by 13%, reaching $82 per barrel—its highest in 14 months. Although it later relaxed to dawn this Monday around $79, the scare was already in the body. This whiplash has had winners and losers in the European stock markets. As you have detailed Guardian, While oil companies (Shell, BP) and defense companies (BAE Systems) rose sharply, airlines such as IAG or easyJet plummeted by around 10% and 7% respectively, terrified by the imminent increase in fuel costs. Moving crude oil today is a high-risk sport. The daily cost of renting a supertanker has skyrocketed by an unusual 600%, reaching $200,000 a day, as Alex Longley warns in Bloomberg. Insurance must be added to this bill: France 24 reports that premiums against war risks They are going to become between 25% and 50% more expensive for those who dare to enter ground zero. The paradox of OPEC+. The next market movement looked askance at the offices. According to the official statement from OPEC+the cartel agreed to inject an additional 206,000 barrels per day starting in April to stabilize prices. However, this measure is, in practice, a logistical mirage. As analyst John Kemp explains: in your column for Finance TimesOPEC+ has excess capacity of more than 3 million barrels per day, but almost all of that capacity is inside of the Persian Gulf countries. In other words, no matter how much extra oil Saudi Arabia or Iraq promise to pump, if the ships cannot cross the Strait of Hormuz, that oil does not exist for the rest of the world. The analysts of wood Mackenzie, collected by oil price, They have been more forceful: “If traffic is not restored quickly, the barrel will pierce the $100 barrier.” The nuances that will define the crisis. Despite the drama, the world has some escape valves that did not exist in the oil crises of the 70s: Lifesaving pipelines: As Kemp explainsSaudi Arabia and the United Arab Emirates can bypass the strait by exporting some of their crude oil through pipelines to the Red Sea and the Gulf of Oman. However, countries like Iraq and Kuwait are trapped: they are 100% dependent on Hormuz. Global shock absorbers: Analyst Javier Blas shells in Bloomberg that the shale revolution (shale oil) in the United States gives Washington unprecedented control over supply. Furthermore, China lIt has been filling to the brim for years its strategic reserves, which would soften the blow in the short term. The big beneficiary: Ironically, the blockade is excellent news for Vladimir Putin. As Blas points outa sustained rise in prices makes it easier for Russia to sell its sanctioned crude oil on the Asian black market with much juicier margins. The world holds its breath. At the moment, the global economy is paralyzed waiting for what a few ship captains decide. Maritime transport giants such as Maersk have already announced the temporary suspension of all their transits through the area, how to collect France 24. Laden ships will remain idle, “avoiding drama,” in the words of a shipping broker consulted by S&P Global. Today, the fate of global inflation is decided not on Wall Street or central banks, but in the tense waters of Oman and Iran, where a swarm of steel giants have decided to shut down their engines and pray for the storm to subside. Image | MarineTraffic Xataka | Tension in Iran is so high that the Strait of Hormuz is closed. And that will have consequences when you go to refuel.