There are numbers that don’t need much explanation. Just take a quick look at them to understand why Warren Buffett has been considered the best investor in history.

The difference between the cumulative performance that have generated the investments that Buffett has made throughout his career as an investor through Berkshire Hathaway, and what it would have meant to invest it in any security in the S&P 500 index during the same time is not a small advantage: it is an abyss.

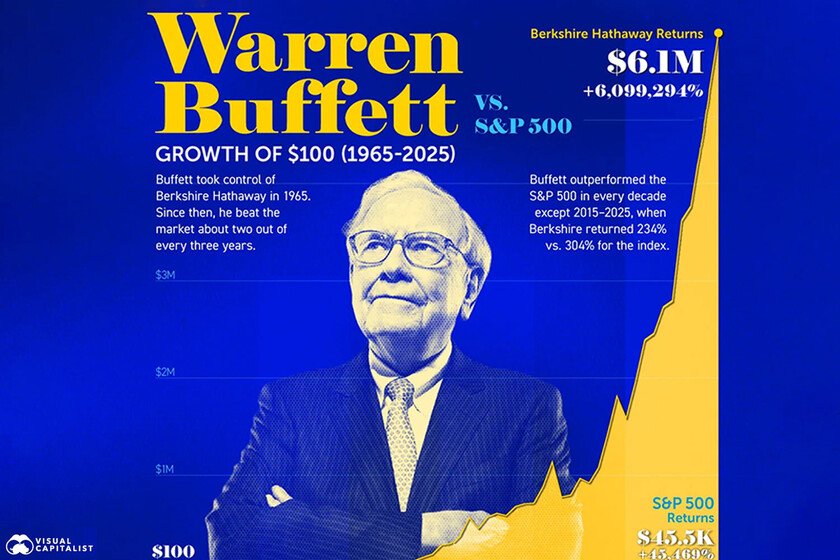

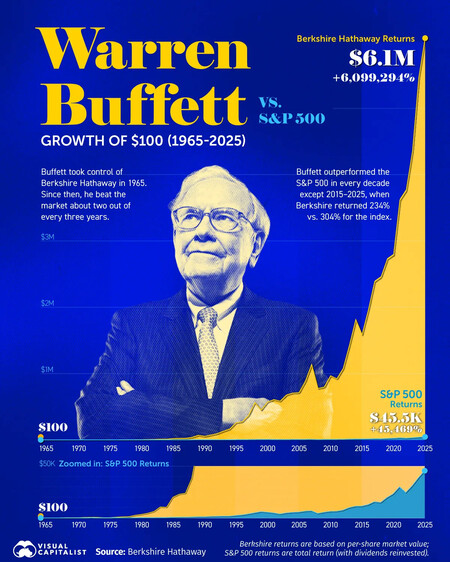

In its traditional letter to its shareholders The company collects on a single page the history of returns obtained since 1965. That page is, possibly, the most eloquent summary of what it means to invest well over a lifetime.

The data portal VisualCapitalist.com has prepared a very illuminating graph with this data and a simple glance is enough to realize the enormous difference between the returns obtained by Buffett and those of the S&P 500. So much difference, that they even had to zoom in on the image so that the evolution of the S&P500 can appear.

Six decades of financial returns

He annual report of Berkshire Hathaway 2025 reflects the evolution of the company’s value per share compared to the performance of the S&P 500 since 1965.

The accumulated result during that period is no less than 6,099,294% for Berkshire, compared to 46,061% for the most followed stock market index in the world. Translated into money, those figures indicate that if you had invested $100 in Berkshire Hathaway in 1965, Buffett would have turned it into more than $6 million today, while that same amount put into the S&P 500 would have grown to just over $46,000.

The compound annual gain that Berkshire has delivered between 1965 and 2025 was 19.7%, almost double the 10.5% achieved by the S&P 500 in that same period. It is not a difference of a few percentage points that accumulate; when we talk about decades, that gap becomes an abyss. He compound interest It has that multiplier effect, and Buffett understood it better than anyone.

Good years and bad years (which are not so bad)

Despite the good historical data for the entire period, not all years ended with green numbers. The table provided by the company each year also reveals that Berkshire Hathaway did not outperform the S&P 500 every year. In 2025, for example, Berkshire’s value per share rose 10.9% while the S&P 500 it did so by 17.9%.

There were other exercises with similar results: in 1967, the S&P 500 index rose 30.9% compared to 13.3% for Berkshire; In 1999, Buffett’s company lost 19.9%, while the S&P gained 21.0%. In 2019, the S&P 500 soared to 31.5%, while Berkshire Hathaway only managed to post a not inconsiderable 11.0% return. Buffett wasn’t playing to win every battle, he was playing to win the war.

But where the veteran investor’s strategy especially shined was when the bad times came. The S&P 500 closed negative 13 times between 1965 and 2025. However, Berkshire weathered the storm better than the S&P 500 in 11 of those 13 years. That is, it lost less during the worst years and even ended positively when everyone lost.

The only two exceptions are found in the results of 1974, in which Berkshire closed the year with a fall of 48.7% compared to 26.4% for the S&P 500, and in 1990, when Buffett’s company fell 23.1% compared to 3.1% for the stock index.

The secret of compound interest

The key to this success in profitability is not in the individual years but in the consistency of the results over time. When an investment grows at a compound annual rate of 19.7% for 60 years, the cumulative effect is exponential: Each year’s profits are added to the previous capital and generate new profits on that growing total. It’s the difference between adding and multiplying, and Buffett made that principle the centerpiece of his entire investment philosophy.

He new CEO of BerkshireGregory Abel, described in his last letter to investors This way of operating compares Buffett with the legendary baseball player Ted Williams, who divided the hitting zone into 77 segments and tried only in a much smaller area, achieving a historical average. “A similar discipline, patience and judgment define Warren’s approach to investing: determine preferred pitches, wait for them, and then strike decisively,” Abel said in the letter to shareholders included in the 2025 annual report.

The Oracle’s investing nose

Abel outlined in the 2025 shareholder letter the philosophy that has guided Berkshire’s investments over the decades, based on moat theory in which capital is concentrated in a small number of companies that understand their business, and defend lasting advantages.

Along these lines, the report highlights Buffett’s historical investments in Apple, American Express or Coca-Cola as the best example of that approach. Businesses that, in Abel’s own words, Berkshire considers to be “companies that we understand well, have great respect for their leaders and have waited for them to grow for decades.”

That investing nose, built with patience and without getting carried away by market fashionsis precisely what has made Buffett a investment legend. Coca-Cola has been in Berkshire’s portfolio since 1988 and American Express since 1991, investments that over time have generated returns that more than multiply the original purchase price. The Oracle of Omaha did not predict the future: he chose well, waited decades and let time do the rest. The same time that has proven him right.

Image | VisualCapitalist

GIPHY App Key not set. Please check settings