Pedro Sánchez announced yesterday Thursday the creation of ‘España Crece’a fund managed by the ICO with an initial endowment of 10.5 billion euros from the Next Generation funds that the Government will not spend before the end of 2026.

The stated goal is to mobilize an additional €120 billion through private investment and debt to maintain the reform momentum beyond the European deadline.

Why is it important. The European funds expire this year and have been the main investment muscle of the Government, which has not approved budgets in this legislature. Without this vehicle, Spain would lose public investment capacity just when Sánchez boasts of having placed the country “in the Champions League” economically.

The announcement arrives in extremiswhen there was a real risk of losing those 10.5 billion that had not been executed.

Between the lines. Calling it a “sovereign fund” creates intentional confusion.

- The classic sovereign funds (Norway, Saudi Arabia, Singapore…) are born from structural surpluses thanks to oil, gas or trade balances that are permanently in the green.

- Spain has not had a budget surplus since 2007, when there was some debate about converting the pension piggy bank into a vehicle similar to Norwegian. The 2008 crisis buried that discussion.

Yes, but. What the Government has presented is more like a renamed investment bank than a traditional sovereign fund. The closest model is British National Wealth Fundoriginally the UK Infrastructure Bank, which raises private funds to co-invest in green technologies and advanced industry. Its capacity is 27,000 million and Spain aspires to quintuple that figure with a smaller public base.

In figures:

- 10.5 billion: initial public endowment, similar to SEPI business rescue fund created in the 2020 pandemic.

- 120,000 million: theoretical capacity if private investment is added, a “conservative estimate” according to Minister Carlos Body.

- 60 billion: what the ICO could mobilize directly through leverage.

- 9 priority sectors: housing (with a focus on the industrialized), energy, digitalization, AI, reindustrialization, circular economy, infrastructure, water and security.

The context. Spain has competed well for foreign direct investment in the last decade – fifth world power in projects greenfield since 2013 – and has capitalized on European funds to promote reforms without approved budgets. But the absence of structural surpluses limits ambition too much.

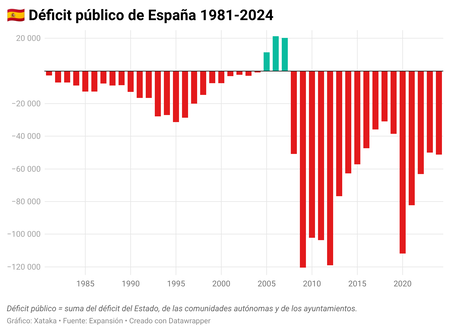

Spain has been running a deficit for almost twenty years and its balance of payments, although in surplus since 2012, does not compensate.

What is happening. The Government is turning a necessity (not to lose unexecuted European funds) into a narrative of national sovereignty. But the seams are visible: it acts because the deadline is going to expire, not because there is a strategic plan based on its own surpluses. There is neither of the two things.

Missing. Minister Corps will present the full details next week. There remain unknowns about the private co-investment mechanisms and how it will be guaranteed that those promised 120 billion will materialize. The experience of the SEPI fund, which barely used a quarter of its endowment, invites skepticism.

Sánchez took advantage of the Spain Investors Day to vindicate the economic moment: “We have become accustomed to competing in the Champions League,” he said. He used the same expression as Zapatero in 2007, a few months before the outbreak of the financial crisis. The simile has not gone unnoticed.

Featured image | Moncloa

GIPHY App Key not set. Please check settings